Gabonds: A Coup in Gabon, a Mistake in DC?

The most important question for Gabon’s future is whether it can pay its debts.

Western Central Africa has seen some of the world’s oldest and longest-ruling leaders – former President Omar Bongo, Cameroon’s Paul Biya, and Equatorial Guinea’s Teodoro Obiang – and is so known for its top-level political stability. In contrast to recent coup victims Burkina Faso and Niger, Gabon’s recent transition from its long-serving familial autocracy to military rule has seen its new rulers project restraint and continuity. An August 2023 coup in Gabon may threaten to upend this stability. Gabon’s new junta has promised modest political change and accused the preceding regime of corruption. At the same time, it is increasing its fiscal expenditure to buy loyalty and put control of the oil and gas industry in state hands.

As a country on the coast of Central Africa bordering Equatorial Guinea, Cameroon, and Congo-Brazzaville, Gabon maintains a low presence in international media. Despite this, it is one of Africa’s richest countries in GDP per capita terms, at $22,000 in per capita purchasing power parity terms. It is a prototypical primary commodity exporter – more than two-thirds of its export earnings are from unrefined petroleum and the rest from manganese ore and timber. Somewhere between a third and half of its government revenue comes from royalties on petroleum exports. The country is one of Africa’s most sparsely populated, with 80% of its 2.4 million citizens living in cities and the rest of the country mostly untouched rainforest.

From 1966 to August 2023, the country was ruled by former President Omar Bongo and his son, Ali, who had succeeded Omar as president in 2009. This continuity was supported by the sanguine position of the foreign oil firms operating in Gabon and a close alignment with France, which maintains a military base in the capital, Libreville. Ali Bongo sought a third presidential term in the 2023 elections and on 30 August obtained a clearly fraudulent result. On the same day, the Gabonese army seized several locations in Libreville, culminating in a 1 September announcement of a coup d’état by General Brice Oligui Nguema, Bongo’s cousin.

Oligui declared the formation of a Committee for the Transition and Restoration of Institutions (CTRI), the suspension of all state institutions, and the president's deposition. This was almost certainly coordinated with Paris – Oligui received the French ambassador and the head of the DGSE on the following day. Two months afterward, Oligui was sworn in as ‘interim’ president and formed a government. The CTRI junta immediately issued several directives, including a constitutional convention, civilian elections in 2025, a new penal code, and a political prisoner amnesty. These are a polite obfuscation of Oligui’s coming electoral coronation – the formal structures of personalist autocracy can be plastic if the autocrat is able to avail himself of a stream of foreign currency and count on the loyalty of the security forces.

The most important question for Gabon’s future is whether it can pay its debts.

The most important question for Gabon’s future is whether it can pay its debts. Oligui inherited a highly burdened balance sheet, with a debt to GDP of 70.5% (113% of non-oil GDP). The IMF estimates it will reach 78.5% by the end of 2024. Debt service is set to consume around 70% of state revenue. Unlike anti-French ‘sovereigntist’ coup leaders in the Sahel, Oligui has not toyed with repudiating these debts. Instead in February 2024, the CTRI announced a National Transition Development Plan (PNDT) for 2024-2026 consisting of an additional $4.9 billion USD (~22% of GDP) in borrowing. Though the junta has not been clear on its plans, this is potentially an addition to the 2024 budget, which already provides for a 12% increase in the public sector wage bill, a 67% increase in public investment and the return of industrial fuel subsidies, which as of their cancellation in 2022 consumed .7% of GDP. The fiscal deficit is projected to rise to 3.8% by the end of 2024 and to 5.1% in 2025, from a low of 1.8% in 2023.

This public spending has been used to stealthily (re-)nationalise large sectors of the economy. The Gabon Oil Company (GOC) announced in January it would pre-empt the previously agreed sale of oil producer Assala to French firm Maurel and Prom from its owners Carlyle Group. Rather than the agreed $700 million, the GOC agreed in February to a $1.3 billion purchase with $800 million of backing from Gunvor Group. Analysts note that Gunvor, as an oil trading house, does not normally provide financing of this type. It is possible some of the shortfall came from a secret Chinese loan. Shortly before his overthrow, Ali Bongo had announced his intention to allow a Chinese military base, and although it has since officially abandoned this ambition, private sources indicate that Chinese diplomatic and financial influence is still present in the country. Neither Gunvor nor Gabon have released the details of the loan, the repayment method, or Gunvor’s role in facilitating or financing it.

The Gabonese government has continued with deals even more dubious than overpaying $500 million for ailing oil assets. Starting in January, it bought 35% of Ceca-Gadis, a national retail firm, and began partial nationalisation of hotels, road haulage, and the country’s manganese miner. In mid-2024, the government acquired a 56% state in the private air travel firm Afrijet, intending to create a national airline. Insider reporting indicates this is part of an ongoing scheme to plunder the assets of the holding company and former Bongo family personal vehicle Delta Synergie. Gabon has not revealed the financing details for these transactions.

The first cracks in the junta’s spending agenda began to show in early June. Moody’s downgraded Gabon from Caa1 to Caa2, two steps above its lowest ranking. In late June, Gabon failed to pay a $17 million payment to the International Bank for Reconstruction and Development (IBRD), causing the World Bank, the IBRD’s parent agency, to suspend disbursal of further funds. This came shortly after the IBRD authorised a $113 million loan to Gabon for government digitisation. After the suspension was leaked, Minister Charles M’ba claimed the non-payment to be a ‘technical’ issue; the IBRD confirmed it was cured three days later.

Nevertheless, it is clear that Gabon is facing debt challenges with the government’s large-scale spending, and this will be tested at the latest in 2025 – Gabon has a 6.95% $700 million dollar-denominated Eurobond due June 2025, of which $600 million remains whose repayment is increasingly in question, as evidenced by the rating agency Fitch downgrading of Gabon from B- to CCC+ on 26 July this year.

More remarkable is that just two weeks before the August 2023 coup, Gabon received strong support from the United States to help manage its debts. Washington’s Development Finance Corporation (DFC), after some two years of cooperation with the Gabonese authorities, agreed to provide political risk insurance policy to a Gabonese ‘blue bond’ – a financial instrument that includes terms of default tied to Gabon’s commitment to protecting its offshore waters. The Nature Conservancy also worked together on the deal, just the third such sovereign blue bond to have been issued, after Belize and Ecuador.

The bond – also referred to as a debt-for-nature swap – saw Gabon raise $500 million dollars. In exchange, it pledged to spend at least $125 million to strengthen fishing regulations and expand its marine nature reserves. However, the majority of the funds raised were used to buy back Gabon’s existing bonds, paying down their principal to lower borrowing costs. The vast majority of this went to paying back two other Eurobonds that Gabon has due in 2031, while some $95 million of the 2025 note was already bought back. Other than the blue bond – which matures in 2038 – that leaves Gabon’s Eurobond indebtedness at $605 million remaining in 2025 and $1.4 billion due in 2031.

The key saving of the Gabonese blue bond came in its coupon, at just 6.097% despite its fifteen-year maturity. With the DFC guarantee, it received a credit rating of Aa2 from Moody’s, which alongside the aforementioned Fitch is one of the three major ‘global standard’ credit rating agencies. That coupon rating is far closer to what the United States would have to pay to borrow than Gabon would have to pay on its own, which would likely have been well over 10%, given the high interest rate environment at the time. This is evidenced by a February 2024 Eurobond issuance by Kenya, rated one notch above Gabon at its issuance. As of the time of writing, Gabon’s Eurobond trades at just a 150-basis point premium to US Treasuries over the same period.

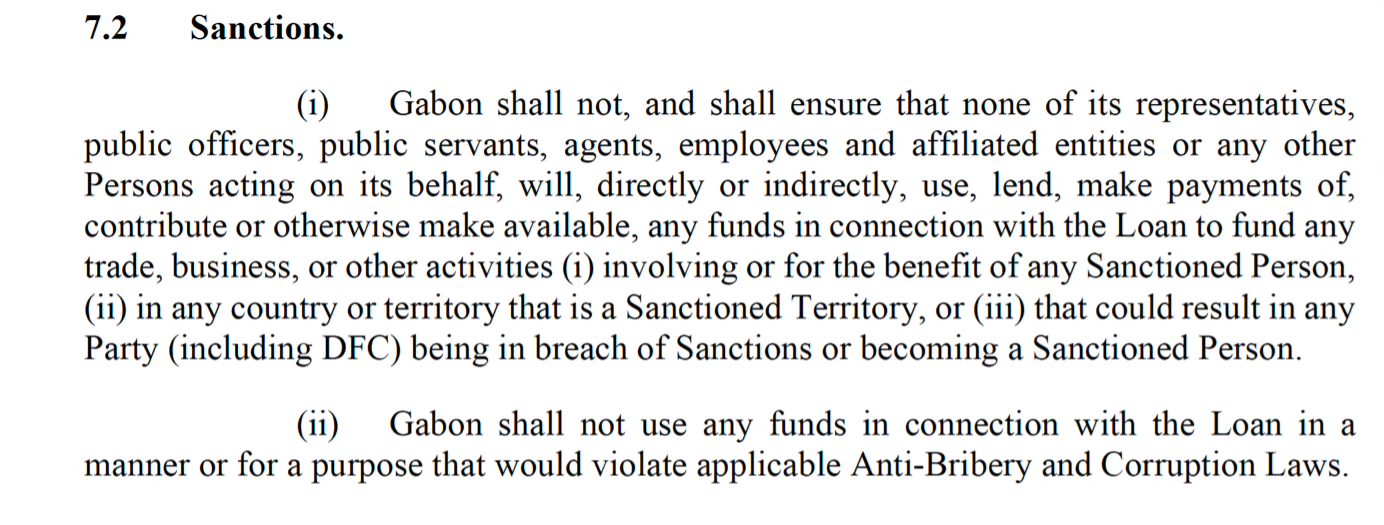

The most damaging provision of the Eurobonds is that the DFC guarantee is voided if Gabon uses the funds raised therefrom to violate US sanctions. And there is ample evidence that Gabon under General Oligui has been doing precisely that.

But therein lies the risk to investors, who are – given the attractiveness of the DFC guarantee – largely insurers and pension funds rather than Emerging Market focussed funds. The Gabonese Blue Bonds contain provisions that determine whether the DFC coverage remains valid. And since the coup, Gabon has not always acted in line with US interests, raising the question of whether Washington will seek to review these terms.

The most damaging provision of the Eurobonds is that the DFC guarantee is voided if Gabon uses the funds raised therefrom to violate US sanctions.

And there is ample evidence that Gabon under General Oligui has been doing precisely that. Gabon’s flag in early 2024 became the favoured ‘flag of convenience’ for Russia’s shadow fleet, which has helped the Kremlin to evade the G7 oil price cap imposed in December 2022. The cap was put in place to try to limit the revenues that Moscow earns from its international oil sales and thus the financing of President Vladimir Putin’s war machine. The European Union and the United States have both since sanctioned numerous tankers that they have identified as sailing under the Gabonese flag.

There are also other indications that not all is well in the relationship between the West and Gabon. In February 2024, the Wall Street Journal published an article claiming that former president Bongo had offered Beijing a deal a year earlier, where Gabon would receive Chinese financing in exchange for offering its territory as a friendly port to China, potentially even for its Navy. The article quoted an unnamed US national security official as saying, “We’re confident that Gabon is not going to permit a permanent PLA presence or establish a Chinese military facility”. China is Gabon’s major trading partner, and the country is also a key source of manganese exports to Beijing. But the US officials’ statement was notably circumspect, and the CTRI junta led by Oligui has continued to hold talks about expanding ties.

And Beijing is unlikely to be scrupulous about whether Gabon honours the terms of its blue bonds. The junta may not be as well. The post-coup transition has largely sought to follow the model of the 2018 Zimbabwe coup by Emmerson Mnangagwa against his former benefactor, longstanding dictator Robert Mugabe: blaming the former president’s family, but not seeking to engage in any kind of radical change. Bongo’s wife was arrested and his son Valentin was charged with extensive corruption. The one other official who has been a major target of the CTRI junta’s ire has been Bongo’s former Environment Minister, Lee White. A Scottish native, according to a 2019 interview that White gave to the Thompson-Reuters Foundation, he became a dual national of the country more than a decade prior, having also served as a conservationist under Omar Bongo before his death and Ali’s succession.

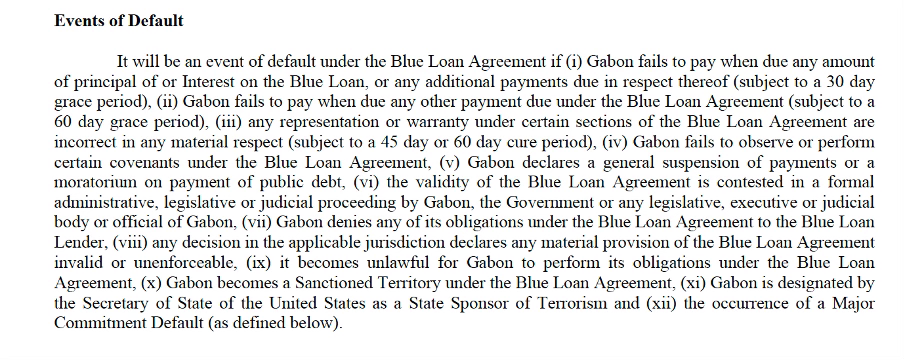

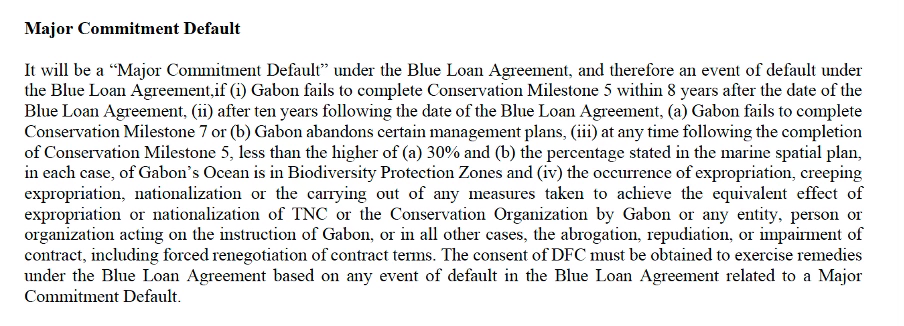

Gabonese media has since dubbed White the “Satan of the waters and forests,” though it did allow him to return to the United Kingdom. Combined with the Assala deal, this is hardly a ringing endorsement of Gabon’s commitment to the bond’s environmental terms. However, the CTRI junta can sit comfortably on the cheap financing that Washington has provided for at least a few more years. The terms of the blue bond do not include the standard cross-default terms of Gabon’s aforementioned three remaining standard sovereign Eurobonds, and while failure to honour the environmental commitments can trigger a default, the first trigger for such an event is only in 2032.

Nevertheless, it is increasingly clear already that it was a mistake for the DFC to offer a guarantee for the blue bond. The timing of the coup, which came just two weeks thereafter, is inauspicious at best, or at worst leaves Washington as an enabler of elite and regime infighting, rather than promoting democracy or human rights. It is also at risk of having enabled one of the most egregious cases of ‘greenwashing’ in any emerging market.

How can Washington address this mistake? How can Washington also pressure Gabon not to continue enabling sanctions violations regarding Russia’s ‘shadow fleet’? Simply put, it must be made clear that the contractually agreed terms of the blue bond are strong, including invoking the DFC’s right to withdraw support if these violations continue.

Image: Adobe Stock